Greenhouse gases (GHG) emission Investorization

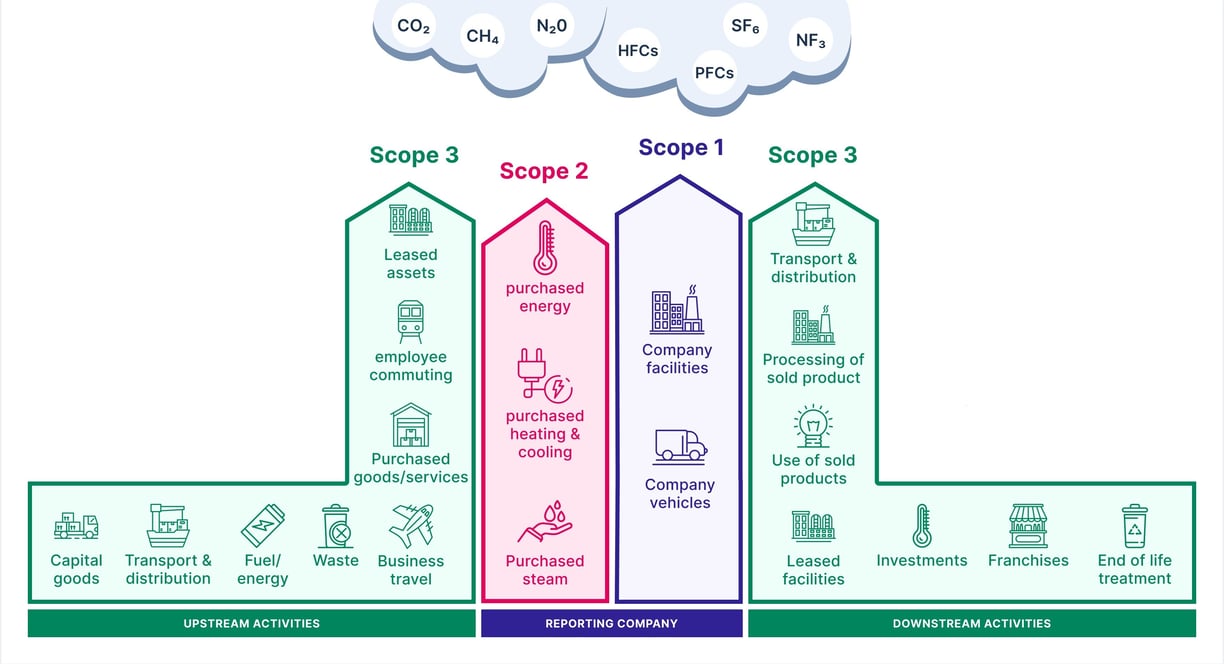

Greenhouse Gas (GHG) Accounting is the process of measuring, managing, and transparently reporting emissions from organizations, activities, or events, guided by standards like the GHG Protocol and ISO 14064.

It categorizes emissions into Scope 1 (direct emissions), Scope 2 (indirect emissions from purchased energy), and Scope 3 (all other indirect emissions across a value chain).

What is GHG Accounting?

Why is GHG Accounting crucial?

GHG Accounting helps organizations understand their carbon footprint, enabling effective emission reduction strategies and ensuring regulatory compliance.

It also identifies inefficiencies, leading to cost savings and improved financial performance while benefiting the environment.

GHG Accounting : Regulatory requirement

Greenhouse gas (GHG) emission reporting is a critical regulatory requirement worldwide, aimed at monitoring and mitigating climate change. Many countries have established mandatory reporting frameworks for businesses, particularly in high-emission industries

Challenges of Scope 3 emissions accounting and reporting

Key challenges of Scope 3 emissions accounting are associated with inaccessibility of information, confidentiality concerns, need for alignment with diverse suppliers, and unscalability.

First, a vast majority of organisations only have access to their direct suppliers, while Scope 3 emissions calculation requires wide-scale data exchange between various value chain actors, including consumers. For example, when calculating downstream emissions, a plastic resin producer is not aware what their product will become (a toy or a food container) and where it will finally end up (incinerated, recycled, or other).

Second, the need for data exchange raises concerns about trust, confidentiality, and privacy. This issue is most prominent for the upstream supply chain actors who have to maintain trade secrets.

Third, the alignment on Scope 3 interventions, terminology, and sustainability metrics between supply chain partners takes time.

Finally, the data management systems are usually either non-existent or unscalable, with information required for GHG accounting often being shared manually through numerous files, surveys, and emails. Establishing such systems might be time-consuming and expensive.

At the same time, knowing the upstream and downstream emissions is essential to calculating and reducing a company’s negative impacts because as much as 85-95% of corporate GHGs originate in the value chain.